⚠️ Flash Flood Warning for Medina, TX — document NOW for NFIP claimsFlood damage guide →

⚠️ Flash Flood Warning for Uvalde, TX — document NOW for NFIP claimsFlood damage guide →

Disaster

How Long Does Storm Damage Roof Replacement Take? The 2026 Timeline by Damage Tier

The most-asked question after a storm-damaged roof claim: "how long until it's done?" Honest answer for 2026: 5 days to 9 months, depending on damage severity, insurance complexity, materials availability, and how thick the post-storm contractor backlog is. Most homeowners assume "a week" — and are blindsided when the calendar slips to month 4. Here's the realistic 2026 timeline breakdown by damage tier, including each phase, what causes delays, and how to compress weeks out of the schedule.

Tier 1 — Minor damage, no insurance claim: 5-14 days

Repair-only work that doesn't require an insurance claim — a few missing shingles, gutter damage, repairable flashing. Cash-pay job.

- Day 1: Inspection + verbal quote.

- Day 2-3: Written estimate.

- Day 4-5: Contract signed, deposit paid.

- Day 7-12: Materials delivered, work scheduled.

- Day 13-14: Install complete (typically 1-day job).

Compression options: pay 50% deposit instead of standard 30%, accept next-available scheduling without negotiating preferred days, use in-stock shingles instead of special-order colors.

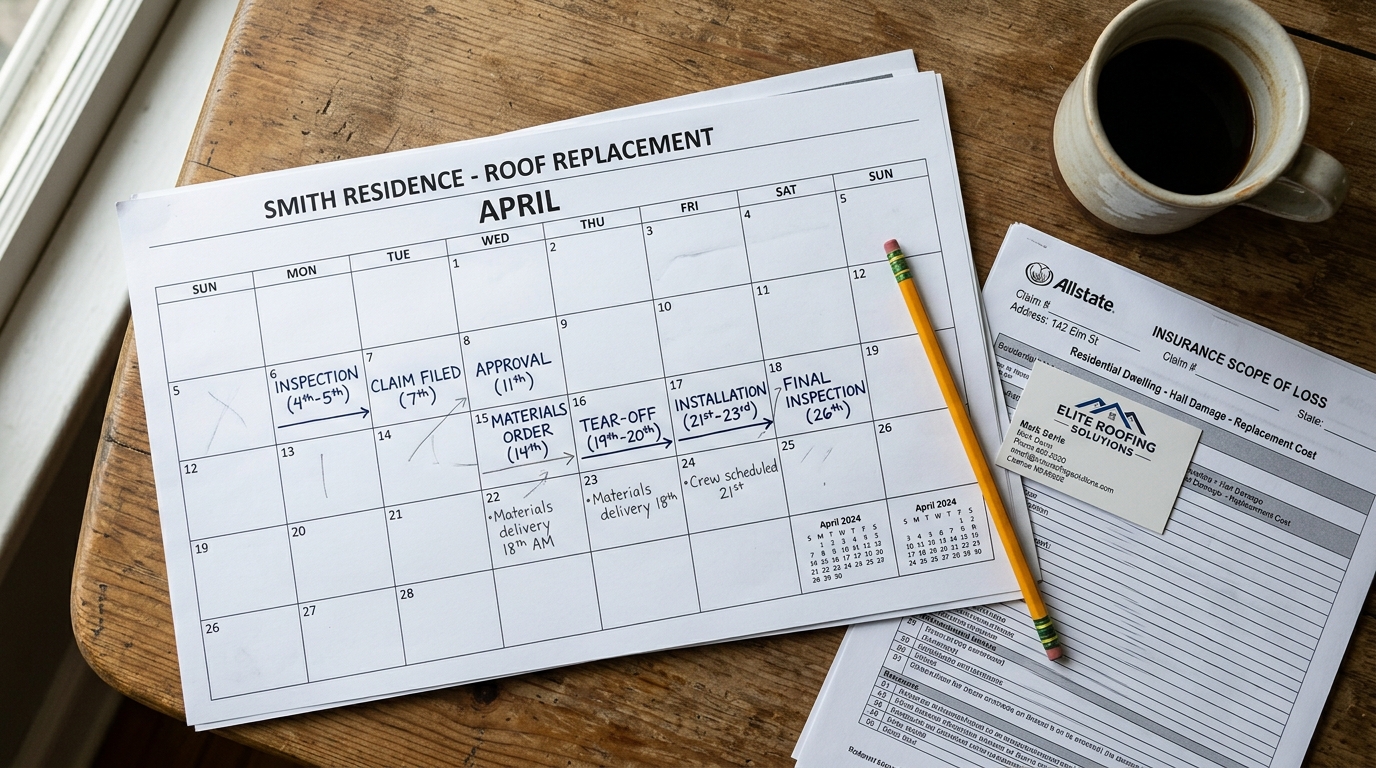

Tier 2 — Minor insurance claim, simple approval: 3-6 weeks

Insurance claim for clear hail/wind damage on a recent-build home (under 10 years old, modern shingles in stock).

- Week 1: Damage event → document → contractor inspection → file claim.

- Week 2: Adjuster visit + on-site contractor assistance.

- Week 3: Receive scope-of-loss. Review + accept (or file minor supplemental).

- Week 4: Sign conditional contract. Receive ACV check from insurance.

- Week 5-6: Materials delivered, install scheduled.

- Week 6 end: Install complete. Submit final paperwork to recover RCV depreciation hold-back.

Get a realistic cost estimate to compare against insurance scope

Same arithmetic this guide uses — adjusted for your roof size, pitch, and quality tier.

Calculate my roof replacement →Tier 3 — Moderate damage, supplemental claims required: 2-4 months

Hail damage on tile roof, older home with code-upgrade requirements, or post-major-storm contractor backlog.

- Week 1-2: Document, inspect, file claim.

- Week 3-4: Adjuster visit. Initial scope-of-loss typically under-scoped.

- Week 5-7: File supplemental claim with contractor documentation (most claims see 15-40% scope increase on supplementals).

- Week 8-9: Receive revised scope + accept.

- Week 10-12: Materials ordered (tile or specialty shingles can be 4-8 weeks lead time).

- Week 13-16: Install scheduled around contractor backlog (post-major-storm contractors are booked 8-14 weeks).

Compression options: choose in-stock material colors, accept a smaller local contractor (often faster scheduling than major firms), pay cash for permit expediting where available, file the most thorough documentation possible upfront to minimize supplemental cycles.

Tier 4 — Major damage, structural work + permits: 4-9 months

Truss damage, decking replacement, code-upgrade work, partial wall damage. Often the case for EF-1 tornado or Cat 2+ hurricane impact.

- Month 1: Document, file claim, secure temporary tarp + water mitigation, file Additional Living Expenses (ALE).

- Month 2: Adjuster visit + structural engineer assessment (for truss/wall damage).

- Month 3: Scope-of-loss + multiple supplementals for code upgrades, structural repairs, Ordinance & Law claim filing.

- Month 4: Permit filing with municipal building department. Plan review + revisions (typical 4-8 weeks).

- Month 5: Materials ordered. Lumber + specialty materials can be 6-12 weeks lead time post-major storm.

- Month 6-8: Structural work + truss replacement + decking + new roof install.

- Month 9: Final inspection, RCV depreciation recovery, ALE close-out.

Tier 5 — Total loss or near-total: 12-22 months

Wildfire total loss, EF-3+ tornado, Category 4-5 hurricane direct hit. Full rebuild.

- Months 1-3: Insurance claim filing, FEMA registration, ALE setup, contents inventory.

- Months 4-6: Adjuster scope, supplementals, debris removal (often EPA-funded for declared disasters).

- Months 7-9: Architect / designer work, permit submission, permit review.

- Months 10-12: Foundation + framing.

- Months 13-15: Mechanical rough-in (electrical, plumbing, HVAC), insulation, drywall.

- Months 16-18: Finishes (flooring, cabinets, fixtures, paint).

- Months 19-22: Punch-list, final inspection, certificate of occupancy.

See our disaster rebuild cost guide for the financial structure of these multi-year rebuilds.

The 6 biggest causes of delay

- Post-storm contractor backlog. After a major event, every contractor in the region is booked 8-14 weeks. The fix: book your contractor BEFORE finalizing your insurance settlement (with a contingent contract).

- Adjuster scheduling. Post-storm, adjusters handle 60-80 claims/week vs. 15-20 normally. Initial visit slipping from 5 days to 3 weeks is common. The fix: file claim within 24-48 hours of the event, before the queue builds.

- Supplemental cycles. Each supplemental claim adds 2-5 weeks. The fix: file ONE comprehensive supplemental with all code-upgrade items, structural items, and contractor documentation rather than multiple smaller ones.

- Materials supply chain. Tile, specialty shingles, custom-color metal, impact-rated windows all see 4-12 week post-storm lead times. The fix: accept in-stock equivalents where possible, or order materials BEFORE contract signing using your contractor's purchasing power.

- Permit delays. Major-storm jurisdictions sometimes waive permits or fast-track them; others overwhelm with volume. The fix: hire a contractor with established relationships at the local building department.

- Weather delays. Roofing requires dry conditions. Post-storm, weather windows close fast. Each rain delay adds 3-5 days.

How to compress your timeline — 6 actions that save weeks

- Document in 24-48 hours, not week 1. Earliest filing = earliest position in adjuster queue.

- Get a contractor inspection BEFORE filing. See our step-by-step claim guide. Filing a borderline claim only to be denied delays you 4-8 weeks.

- Have your contractor present at the adjuster visit. Reduces supplemental cycles by 60%+.

- File ONE comprehensive supplemental covering all code upgrades, structural items, code-upgrade Ordinance & Law claim, and contractor scope additions — instead of 3-4 smaller ones.

- Accept in-stock materials where reasonable. A 4-week lead time on a specialty shingle color isn't worth slipping 4 weeks late.

- Pre-book your contractor with a contingent ("subject to insurance approval") contract during week 2-3. Don't wait for the final scope to start contractor selection.

Why timeline matters financially

- ALE expiration: most policies cap at 12-24 months. Slipping to month 25 on a 22-month rebuild = $20K-$40K of out-of-pocket housing.

- RCV recovery requirement: insurance pays RCV depreciation only AFTER install + paperwork. A 4-month delay = 4 months sitting on the ACV check vs. having full RCV.

- Materials inflation: 2025-2026 saw 6-12% material cost increases. A 6-month delay between estimate and order can leave the supplemental scope underwater.

- Insurance non-renewal risk: if your roof slips past the carrier's age-cap during the delay (rare but happens), your renewal gets non-renewed before the replacement completes.

Trusted timeline + claim guidance

- How to file a roof insurance claim step by step

- Does homeowners insurance cover roof replacement?

- Storm-chaser roofer scams — how to avoid them

- Texas hail damage guide

- Florida hail damage guide

- Tornado damage home repair cost

Bottom line

Storm damage roof replacement runs 5 days (minor cash-pay) to 22 months (total loss rebuild) depending on tier. Most claimants are in Tier 2-3 (3-6 weeks for clean claims, 2-4 months when supplementals + code upgrades are involved). The 6 time-savers: document in 24-48 hours, contractor inspection before filing, contractor present at adjuster visit, ONE comprehensive supplemental, accept in-stock materials, pre-book contractor with contingent contract. Each delay costs real money — ALE expiration, RCV hold-back, materials inflation, insurance non-renewal risk. Use our state-specific roofing calculators to know your real replacement cost before insurance scopes the claim.

Get 3 free contractor quotes for your storm-damaged roof

Vetted local roofers who handle insurance claims. No spam, no obligation, no sales calls — we just send the quotes.

Most homeowners receive 3 quotes within 48 hours. Free service — funded by contractor referral fees, not by you.